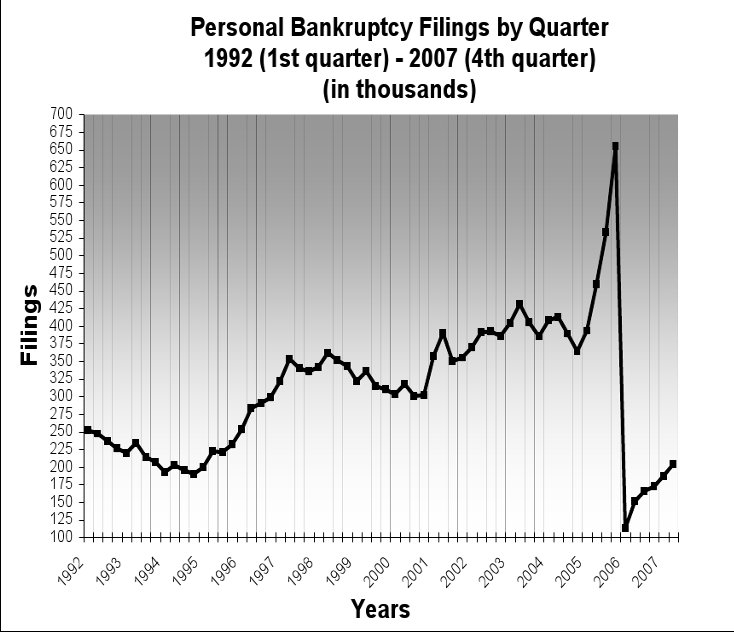

Bankruptcy Overview

Sometimes you may find yourself overwhelmed with bills, debts, and creditor’s calling to collect on those debts. Are you behind on your mortgage, car payments, or have you recently faced an overwhelming medical bill or lawsuit that threatens to wipe out your finances? Is your business in need of debt restructuring so that it can continue operations? If so, bankruptcy may be an option you should seriously pursue before matters become worse.

Federal bankruptcy law exists to give debtors a “fresh start” from burdensome debts. That goal is accomplished through the bankruptcy discharge, which releases debtors from personal liability from specific debts, and prohibits creditors from ever taking any action against the debtor to collect these debts.

The Bankruptcy Code provides several options for debtors to obtain this “fresh start,” Chapter 7, Chapter 11, and Chapter 13. Each is appropriate for different circumstances. Chapter 7 allows an individual debtor to discharge certain debts, while an appointed trustee sells off assets to pay off debts. A business may also file a Chapter 7 petition, which will close down the business. Chapter 13 bankruptcy is appropriate for an individual who intends to reschedule his debt for repayment over a period of time, rather than liquidating his assets like in Chapter 7. Chapter 11 bankruptcy is for a corporation seeking to reorganize its debt in order to continue operations. In Chapter 11, the debtor generally keeps control over the business.

Bankruptcy is a serious option that you need to consider wisely before undertaking. You need to understand the consequences of bankruptcy, and how it will affect your credit after the proceedings. RobertsMiceli LLP is ready to discuss your options and what will be required of you during the proceedings, as well as the consequences after the bankruptcy discharge.

Related Content

- Bankruptcy Overview

- Official Bankruptcy Forms

- Creditor's Rights

- Bankruptcy FAQ

- Preparing to Meet with a Bankruptcy Lawyer

- The U.S. Bankruptcy Trustee Program